Individual Savings Accounts

Look to the future and start saving today - It's never too late to start

Reminder - tax year end fast approaching

5th April 2023 is the deadline for using your ISA allowance is 5th April 2023. This is the end of the tax year and after this date your tax-free ISA allowance for 2022/23 is gone.

An individual savings account lets you earn interest on cash savings or investments without paying any income tax, but you are limited by how much you can put in. Here’s everything you need to know to get started.

ISAs were introduced more than two decades ago to encourage people to save for their future. What an ISA account is has changed a bit over the years, but essentially, they can be used to save cash, lend money or invest in the stock market in a tax-efficient way.

How do ISAs work?

Every tax year, which runs from 6 April to 5 April the following year, you are given an ISA allowance that lets you save or invest money up to a certain amount without paying tax on your returns.

Your ISA allowance for the 2021/22 tax year is £20,000. This means you have until 5 April 2022 to use up your ISA allowance for this tax year.

If you miss this deadline, any money you pay into an ISA will count towards your 2022/23 ISA allowance.

How much tax do you save with ISAs?

You will not pay any income tax on money saved in an ISA, providing you don’t pay in more than your allowance each tax year. If you are over-enthusiastic with your ISA deposits, HMRC will let you know what you owe in tax. The amount you would repay will depend on your tax-rate status, which for the 2021/22 tax year is:

Updated 22 December 2021

| Type of taxpayer | Income tax on savings | Income tax on ISAs |

|---|---|---|

| Basic rate | 20%* | 0% |

| Higher rate | 40%* | 0% |

| Additional rate | 45% | 0% |

*After exceeding personal savings allowance of up to £1,000 in interest per tax year.

How do ISAs compare

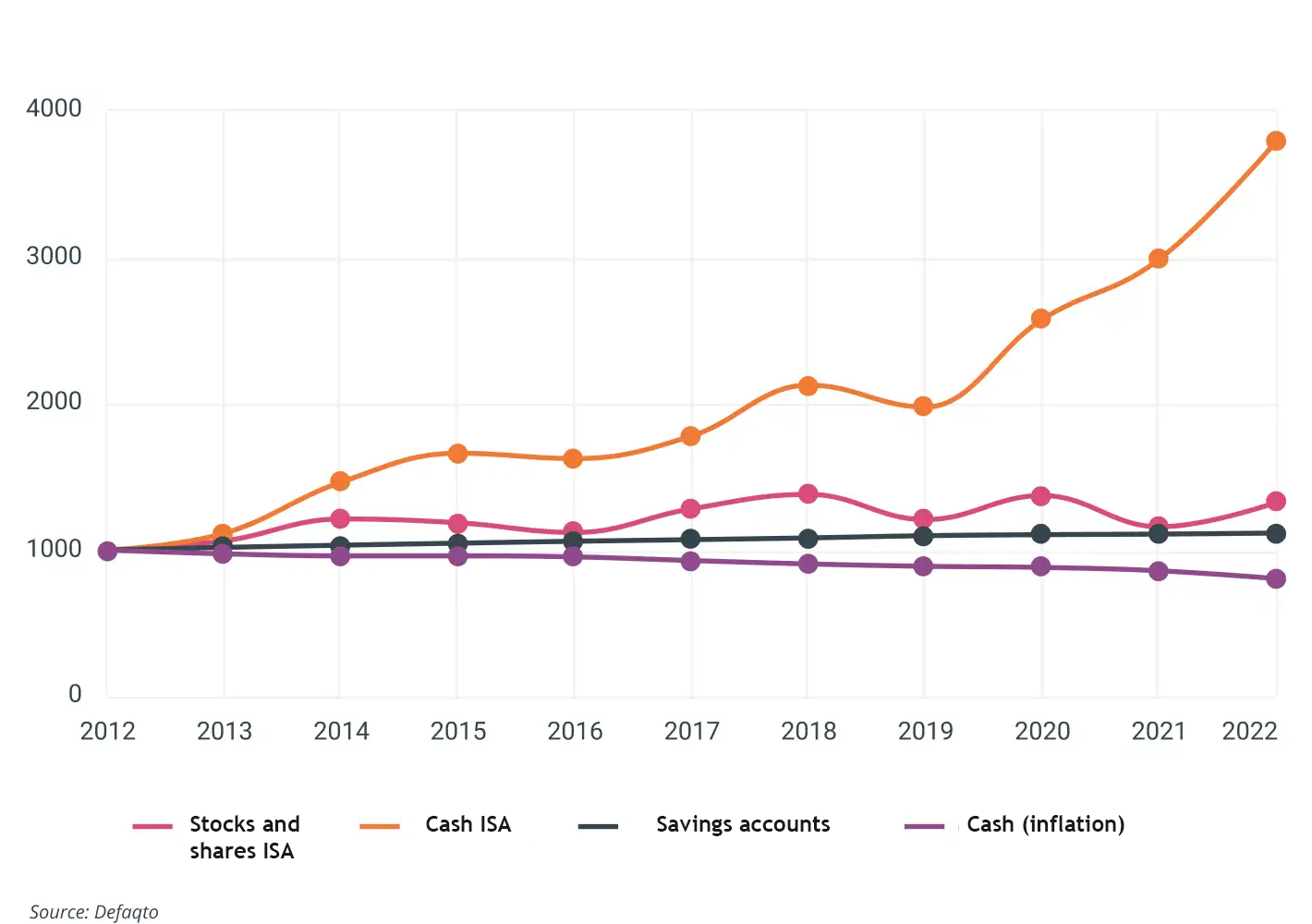

At a time when interest rates are relatively low and inflation running at multi-decade highs, it is understandable that investors are looking beyond cash ISAs. As of October 2022, the best variable cash ISA rate on offer stands at just 2.25%. This level of interest will not protect investors from the ravages of inflation.

In contrast, stocks and shares ISAs provide investors with the prospect of inflation-beating returns over time within a tax-free wrapper. However, the word ‘prospect’ is important here; returns aren’t guaranteed and much will come down to what is in your portfolio. Alternatively, if you appoint a professional to manage your stocks and shares ISA, you are relying on their skill to beat inflation over time.

This can be illustrated by the graph that shows the fourfold returns on stocks and shares ISA products between 2012 and 2022 when compared to lower returns on the Cash ISA at around 3.5% over the same decade.

Our ISA Products

Explore our ISAs to find the perfect for you and your aspirations.

Stocks and shares ISA

A stocks and shares ISA is a tax-efficient investment account that allows you to invest in a range of shares.

From just £20 a month, or a £100 lump sum deposit, you can start saving

- Five diversified fund solutions to choose from based on your risk appetite

- A team of experts actively managing award winning funds

- Our online ISA account helps you to save, tax efficiently

Cash ISA

These work in the same way as conventional savings accounts, but with the tax-free wrapper. There are two basic types of Cash ISA:

- Instant access: You can withdraw and deposit funds

- Fixed term: Your money is tied up for a fixed term

Junior ISA

Junior Individual Savings Accounts (ISAs) are long-term, tax-free savings accounts for children.

There are 2 types of Junior ISA:

- a cash Junior ISA, for example you will not pay tax on interest on the cash you save

- a stocks and shares Junior ISA, for example your cash is invested and you will not pay tax on any capital growth or dividends you receive

Lifetime ISA

You can use a Lifetime ISA to buy your first home or save for later life. You must be 18 or over but under 40 to open a Lifetime ISA.

You can put in up to £4,000 each year, until you’re 50. You must make your first payment into your ISA before you’re 40.

The government will add a 25% bonus to your savings, up to a maximum of £1,000 per year.

Lifetime ISAAre you looking to take the next step?

Get in touch with use to either request a brochure or submit your contact details and we'll get in touch to discuss our ISA products with you to find the perfect fit.

Frequently Asked Questions

You can accumulate several ISAs over the years. And you can also consolidate your past ISAs by transferring them to your current ISAs if they offer more attractive terms.

However, you can only pay into one Cash ISA, one Stocks and Shares ISA and one Innovative Finance ISA in each tax year, and the total you invest across the three types of account must not exceed your ISA allowance – currently £20,000.

If you have opened a Junior ISA for your child, this is treated as outside your allowance (it’s your child’s account and their allowance, which is £9,000 a year for 2021/22).

To be eligible to open an ISA, you need to:

- Be 16 or older for a Cash ISA

- Be 18 for Stocks and Shares ISA or an Innovative Finance ISA

- Be the parent or guardian of a child under 18 to open a Junior ISA

- Be 18 to 39 to open a Lifetime ISA

- Be a resident in the UK (or a Crown employee if abroad)

- An ISA can only be held in one person's name. It’s not possible to have an ISA in joint names.

You can open an ISA in a branch, online, by post or over the phone, depending on the type of account and provider you choose.

You’ll need to put some money in when you open an ISA, meaning you’ll need funds available to cover the minimum amount, which can vary from £1 to more than £1,000.

You’ll need to give your personal details when you apply, including your:

- Name

- Address

- National Insurance number

You’ll need to read an ISA declaration, which tells you how ISAs work.

Read the application form carefully before signing, as it may include details of important restrictions such as withdrawal penalties.

You’ll be given a passbook, certificate or an online statement to view after you open your ISA.

When it comes to managing your account, you’ll need your passbook or certificate to make any withdrawals or changes to your account if you have a branch-based ISA. You can usually manage online ISAs via your computer, tablet or mobile phone.

Your ISA is flexible

You can withdraw money and pay it back in during the same tax year without it affecting your ISA allowance (e.g. if you deposit £5,000 then withdraw the same amount, you can still pay in a total of £20,000 this tax year)

You can also withdraw any ISA money you have from previous tax years, and have until the end of the tax year to pay it back in

In both cases, check the small print before doing anything as some ISAs limit the number of transactions you can make. As not all ISA providers allow transfers, you should also check the T&Cs before making a withdrawal.

Your ISA is not flexible

Any money you pay in then withdraw will still count towards your remaining ISA allowance (e.g. if you pay in then withdraw £5,000, you can only deposit up to £15,000 for the rest of this tax year).

Deposits that exceed the allowance will generally be rejected

Your money will also lose its tax-free status if you withdraw it and pay it into a normal savings account.

When you die your ISA becomes part of your estate and loses its tax-free status, meaning it’s liable to income tax, which will affect what your beneficiaries get.

The exception is if you leave behind a spouse or civil partner. In this case, they would see an amount equivalent to your ISA savings or investments added to their current year’s allowance, tax-free.

For example, if you die leaving £50,000, your spouse or civil partner would receive a one-off extension to their annual allowance of this sum, giving them a total allowance of £70,000 to invest as they see fit.

Even if you leave your ISA to somebody else in your will, such as your son or daughter, your spouse or civil partner will still benefit from the £50,000 additional ISA allowance.

You may want to move holdings in a previous year’s ISA to a new one if the rate of return is better. This is allowed under the rules; just don’t attempt a transfer until you’ve checked whether your new ISA allows transfers in.

To retain your tax advantages, you need to transfer your ISA directly from one provider to another.

This way, you won’t lose the ISA allowance you had already built up in an old ISA or affect your current year’s allowance. So if you move £20,000 from an old account to a new Cash ISA, you’ll still have up to £20,000 to deposit before the end of the current tax year.

If you want to transfer your ISA to another with the same provider, you can also ask to do an ISA consolidation, which lets you combine ISAs together into a new or existing ISA.

However, if you try to move your ISA by withdrawing the funds, you will lose its ISA status, as it’s no longer within the tax-free wrapper.

The Financial Services Compensation Scheme (FSCS) protects the first £85,000 of any cash or investments held in ISAs with each separately registered institution.

To qualify, your ISAs must be in a financial company, such as a bank or investment house, that’s regulated by the Financial Conduct Authority (you can check whether yours is here).

If you have more than £85,000 in savings with one institution, or two sister companies in the same group, you could end up out of pocket should the group go bust as the FSCS only guarantees a payout of £85,000.